Nurturing financial well-being through retirement savings

Jacqueline Boersema, Director of Financial Education at the Board of Pensions, knows that just like staying physically healthy takes small, consistent steps, so does building financial well-being. She shares how even modest actions — like contributing to a retirement savings account — can make a big difference over time.

It takes effort and diligence to maintain a healthy lifestyle, and the same is true for financial well-being. Financial well-being is something we need to nurture and focus on throughout our lives; fortunately, there are resources that can help.

Just as adding a 10-minute daily walk can improve your physical health, consistently saving — even a small amount — can lead to a financially healthier you. One tool that can help you achieve this is a retirement savings account, such as the

Retirement Savings Plan of the Presbyterian Church (U.S.A.), a qualified 403(b)(9) defined contribution church plan that allows for tax-advantaged savings. If you’re

enrolled in the Retirement Savings Plan, you can take the first step by

contributing to your account or a larger step by increasing your current contribution. Either way, you will be putting in place healthy financial practices that contribute to your financial well‑being.

The Retirement Savings Plan helps you save more because the interest and dividends earned are not taxed annually. This allows your money to grow tax-free until you withdraw it for retirement, which can begin as early as age 55 and, under current IRS rules, must begin by April 1 of the year after you turn 73 — or, if you continue working for a PC(USA) organization, when you actually retire.

For example:

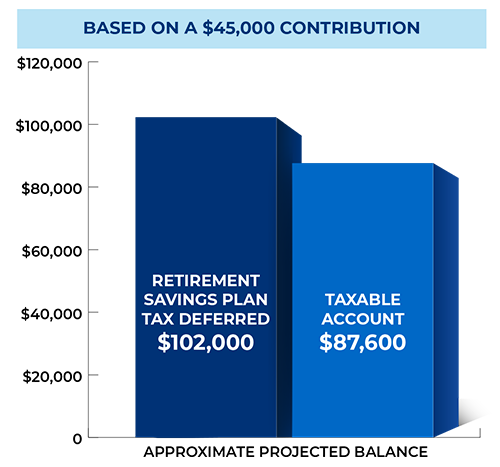

If you contributed $150 per month to the Retirement Savings Plan instead of a taxable account (like a certificate of deposit account) earning 6% over 25 years, your approximate projected balance would be:

In addition, your taxable income would be reduced each year by your contributions to the Retirement Savings Plan. If you are a minister, the amount you contribute would also be exempt from Self-Employment Contributions Act (SECA) tax (a federal tax that covers Social Security and Medicare for individuals who are self-employed, including ministers).

Ready to start a new financial habit?

Take the first step by exploring Fidelity’s retirement planning tools — designed to support your journey whether you're participating in the Retirement Savings Plan or not.

Jacqueline Boersema is Director, Financial Education, at the Board of Pensions. A certified financial planner and a registered investment adviser with 30 years’ financial service experience in private banking and at accounting firms, she is responsible for developing and presenting Lifelong Learning programs addressing the centrality of financial wholeness to our overall well-being, focusing on financial literacy, financial planning, and retirement readiness.

The projections and balances shown are for illustrative purposes only and are based on several assumptions, including a fixed monthly contribution of $150, an annual return rate of 6%, no employer match, and a 25-year investment period. These figures do not account for market volatility, changes in salary, contribution adjustments, or tax law changes. Actual investment results may vary. The purchasing power estimates assume a 3% annual inflation rate. This example does not constitute financial advice and should not be relied upon for retirement planning decisions. For specific advice based on your personal circumstances, you should consult a qualified tax or financial adviser.